September 05, 2023 • 6 min read

Have you ever opened up a credit report PDF for one of your applicants and felt your eyes glaze over like you’re staring at something written in a different language?

Imagine opening any credit report and understanding every line, nook, and cranny at first glance. Even better, what if that report flagged things you might be potentially concerned about? Think of the time you’d save — and the headaches you’d avoid — by reading and understanding the credit report on the first look.

This post will give you that superpower! We will walk you through how to read a credit report PDF like a pro, going through each section and the six key insights you need to remember when reading credit reports.

How To Read a Credit Report PDF

To effectively evaluate a credit report, you need to understand each section. Let’s look at the critical sections of a credit report to give you an idea of what you should focus on when reviewing each section!

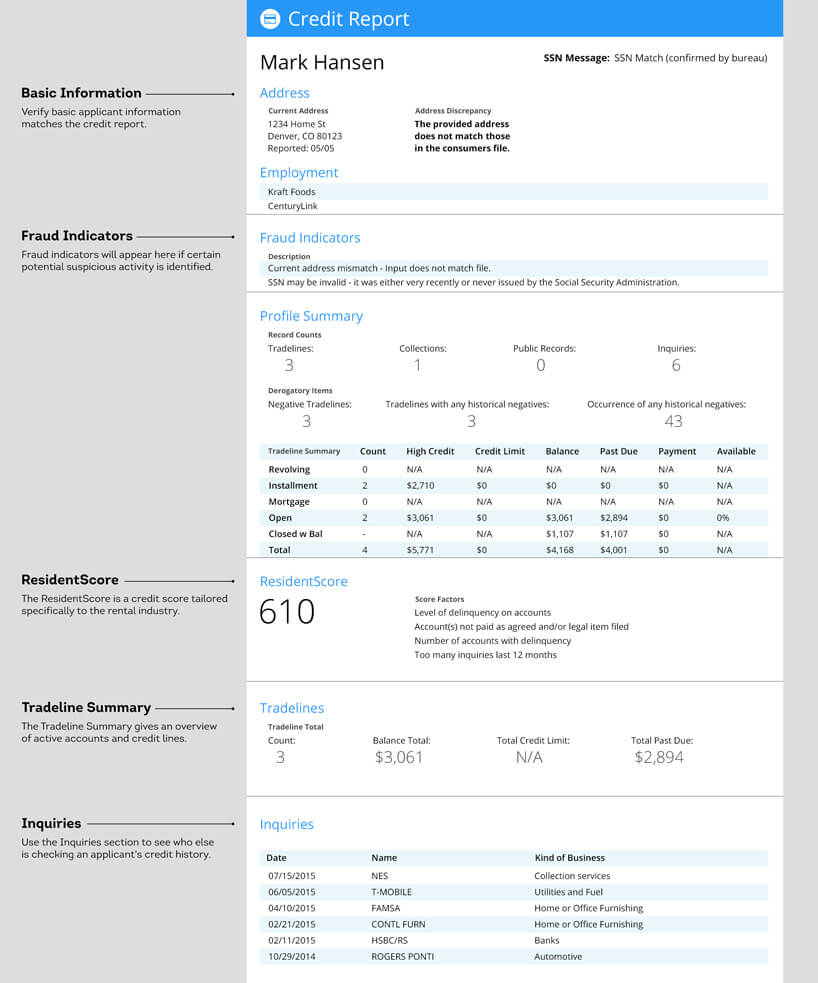

Personal information: In this section, you'll want to verify the accuracy of the applicant's personal details, including their name, address, and Social Security number. It's crucial to ensure that this information matches the rental application and identification documents provided. Any discrepancies could be a cause for concern and warrant further investigation.

Account summary: This section provides an overview of the applicant's accounts. Pay attention to the types of accounts listed, such as credit cards or loans. Take note of the total number of accounts and their status, whether open, closed, or active. Also, look for any accounts reported as delinquent, in collections, or charged off.

Related Read: How to Understand an Applicant's FICO Score

Payment history: This section reveals the applicant's track record of timely payments. Look for records of on-time payments and any late payments, delinquencies, or missed payments. Additionally, take note of accounts that have been sent to collections or charged off, as these indicate potential financial difficulties.

Public records: The public records section provides information on bankruptcies, foreclosures, tax liens, or civil judgments. Reviewing this section gives you an understanding of any significant legal or financial issues the applicant may have faced in the past.

Credit inquiries: This section shows recent inquiries made by lenders or creditors. Multiple inquiries within a short period could indicate potential financial distress or new debt, so it's essential to be aware of any significant changes in the applicant's credit-seeking behavior.

Account details: In this section, consider the creditor's name, account type, and account number. Note the current balance and credit limit associated with each account. This information helps you gauge the applicant's overall debt load and credit utilization.

Credit utilization: You can calculate the credit utilization ratio by dividing the total credit card balances by the credit limits. High credit utilization, typically above 30%, may indicate financial strain or increased risk, so it's essential to assess this aspect carefully.

Account history: This section reveals the applicant's credit history length. A longer credit history reflects stability and responsible credit usage, which can be positive indicators of the applicant’s personal habits and lifestyle.

Dispute statements: These are statements the applicant has added to dispute information on their credit report. Pay attention to their explanations for disputed items, as they can offer valuable insights into any discrepancies or errors.

By carefully reviewing each credit report section, you can understand the applicant's creditworthiness and make well-informed decisions based on their financial history. Let’s now review the six top things you should look out for when reviewing a credit report PDF for tenant screening.

1. Credit Score

The first — and most obvious — thing to look at when examining a credit report is the applicant’s credit score.

This three-digit number summarizes their creditworthiness based on payment history, credit utilization, length of credit history, and types of credit accounts. The higher the credit score, the more confidence you can have in the applicant's ability to pay their rent regularly and on time.

Related Read: How to Screen Tenants for Your Rental Property: 10-Step Guide

In addition to the credit score, pay attention to the applicant's credit history length. Though a longer credit history provides a better understanding of their financial habits and stability, you should keep in mind that a short credit history doesn't necessarily indicate a higher risk, especially for young or first-time renters. If your applicant has a short credit history, consider weighing the credit score less severely than the other items on this list!

2. Payment History

The next section you should consider is the payment history section. This section provides valuable insights into their payment behavior over time. Look for any late payments, delinquencies, or accounts that have gone into collections. Consistently late payments suggest a potential risk for late rent payments, while accounts in collections could indicate ongoing financial struggles.

Another aspect to consider within the payment history section is the applicant's credit utilization ratio. This ratio compares their total credit card balances to their credit limits. High credit utilization, where the balances are close to or exceed the credit limits, may indicate financial strain or potential challenges in meeting financial obligations like rent payments.

3. Outstanding Debts

Assessing the applicant's outstanding debts is another crucial element in evaluating their ability to pay rent. Look for any indications of significant debt, such as credit card balances, student loans, or auto loans.

Consider the applicant's debt-to-income ratio. This ratio compares their monthly debt payments to their monthly income. A high debt-to-income ratio may suggest that a significant portion of their income is already allocated towards debt obligations, leaving less room for additional expenses like rent.

Debt is not uncommon, and it’s important to remember this is just one piece of the applicant’s overall financial puzzle. Where traditional leasing processes may use this as a disqualifier, remember to consider this element in conjunction with the other elements of their credit history for the full picture.

4. Bankruptcies and Foreclosures

Bankruptcies and foreclosures can provide valuable insights into the applicant's financial history. Check the credit report for any past bankruptcies or foreclosures, which may indicate a higher risk of defaulting on rent payments. While everyone faces challenges, property managers must consider the circumstances and the steps the applicant has taken to rebuild their financial situation.

It's important to note that bankruptcies and foreclosures should not automatically disqualify applicants in all cases. Instead, consider this alongside the applicant's overall financial stability, employment history, and any positive steps they have taken toward improving their creditworthiness.

Additionally, look for any records of prior evictions or rental-related judgments. Consistent late payments or disputes with previous landlords could be warning signs of potential issues with meeting rental obligations.

5. Inquiries and Public Records

Credit inquiries and public records provide additional information that can help you evaluate an applicant's creditworthiness. Take note of the number of recent credit inquiries made by the applicant.

Multiple inquiries within a short period could indicate a higher risk of financial instability or potential debt accumulation. Also, check for any liens, judgments, or legal actions against the applicant in the public records section. These records can provide insights into potential financial and legal issues they may be facing. Assess the impact of these records on their ability to fulfill their rental obligations and make timely payments.

6. Identity Verification

Last but not least, ensuring that the applicant's personal information matches the details provided on their rental application is crucial. Verify that their name, address, and Social Security number are accurate and consistent across all documents. Any discrepancies or inconsistencies could be red flags and should be investigated further.

Identity verification is essential for confirming the applicant's identity and ensuring that you evaluate the credit report of the correct individual. It helps prevent fraudulent applications and ensures you make your decisions based on accurate information.

Read Your Credit Report PDFs The Easy Way

You can easily read any credit report PDF by looking out for each section we discussed at the beginning of this post. By keeping these six key insights in mind, you can avoid misunderstandings, misreadings, and other common challenges during credit screening.

Being able to read a credit report is only the first step in your journey to streamlining and optimizing your property management processes. If you truly want to eliminate friction in your leasing process, you need a tool that can help you attract, screen, and compare applicants.

Intellirent allows you to accelerate and simplify your leasing process with easy-to-read credit and background reports, a customizable online application, a centralized collaboration tool, and more.

Schedule a free product tour today to see if Intellirent is the right solution for your property management needs!

Related Articles

September 19, 2023 • 5 min read

March 05, 2024 • 7 min read